Last Week in Review; The Jobs Report

| People say that “life is full of surprises.” And last week’s Jobs Report offered a few surprises of its own. But were those surprises positive, and what do they mean for home loan rates overall? Read on for details.

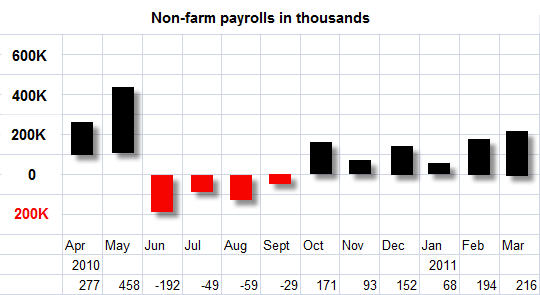

The headline Jobs Report number showed that 216,000 jobs were created in March, which was a positive surprise as this was above expectations. In addition, 230,000 jobs were created in the private sector, which was also better than expectations and offset a decline in government jobs. A small 2,000 upwards revision to February’s prior release added some more jobs as well. In addition, the Unemployment Rate surprisingly dropped to 8.8%, which is the lowest unemployment rate since March of 2009. Remember, the Unemployment Rate is derived from the Household Survey (exactly as it sounds, from calls made to households), and is considered to be more accurate than the Current Employment Statistics or Business Survey (again as it sounds, from calls made to businesses), which is used to determine the headline jobs number. The one negative within the report is Hourly Earnings coming in at 0.0%. This is the second month in a row where earnings growth is 0.0%. Why is this significant? If earnings don’t grow, people have less to spend and as a forward looking indicator on job growth, it shows that businesses are presently not under any pressure to raise wages. This means they may not have to hire new people as quickly because they may have room to raise wages for present workers down the road. Overall, the Jobs Report was a good report and reminds us that the trend in the labor market is improving. But keep in mind, while lowering unemployment is good for our economy overall – as are the other two goals (creating inflation and boosting Stock prices) of the Fed’s current Quantitative Easing (QE2) program – these goals can also lead to higher home loan rates over time. In fact, inflation continues to be a growing concern both around the world and here in the U.S., as several members of the Fed, including St. Louis Fed President James Bullard, have expressed concern that if the Fed waits “too long (to remove accommodative monetary policy) we will get a lot of inflation in the United States and around the world.” What does this mean in the long run? Like the Treasury Department, at some point the Fed will start selling some of its massive holdings and unwind their QE1 and QE2 purchases. And when it does, not only will the Bond market lose a buyer in the Fed, but they will gain a seller and this will make it hard for Mortgage Backed Securities and home loan rates, which are tied to these types of Bonds, to meaningfully improve. If you have been thinking about purchasing or refinancing a home, call or email me to learn more about how you can benefit. Or forward this newsletter on to someone you know who may benefit from today’s historically low rates. |

Ricardo Cobos is a Mortgage Lender in Raleigh North Carolina who expertly assists people who are buying homes in Raleigh and Cary North Carolina (919) -559-3384.

Since relocating from Northern Michigan in 2007 I have lived in Garner (27529) with my wife Melanie and our four children. With personal production of 8MM in real estate sales across Southern Wake County I am considered to be a local market expert in the following communities: Garner (27529), Fuquay-Varina (27526), Holly-Springs (27540), Apex (27502), and Raleigh (27603, 27604, 27606, 27609, 27610)) which spans from downtown Raleigh to Willow Spring including Lake Wheeler. Call or email me, I’m here to help! Ricardo Cobos (919) 526-0183